The oil price keeps falling. And most analysts seem convinced that they know the reason — it’s about supply, or demand, or Putin, or Saudi Arabia, or Syria or…

But what if it were something completely different, known only by top people at the world’s biggest banks. And you. That a new, clean and basically infinite energy source might replace oil (and gas, coal and nuclear).

Torkel Nyberg, who runs the blog Sifferkoll.se, has studied this hypothesis for several years. And half a year ago he got what looks like a smoking gun.

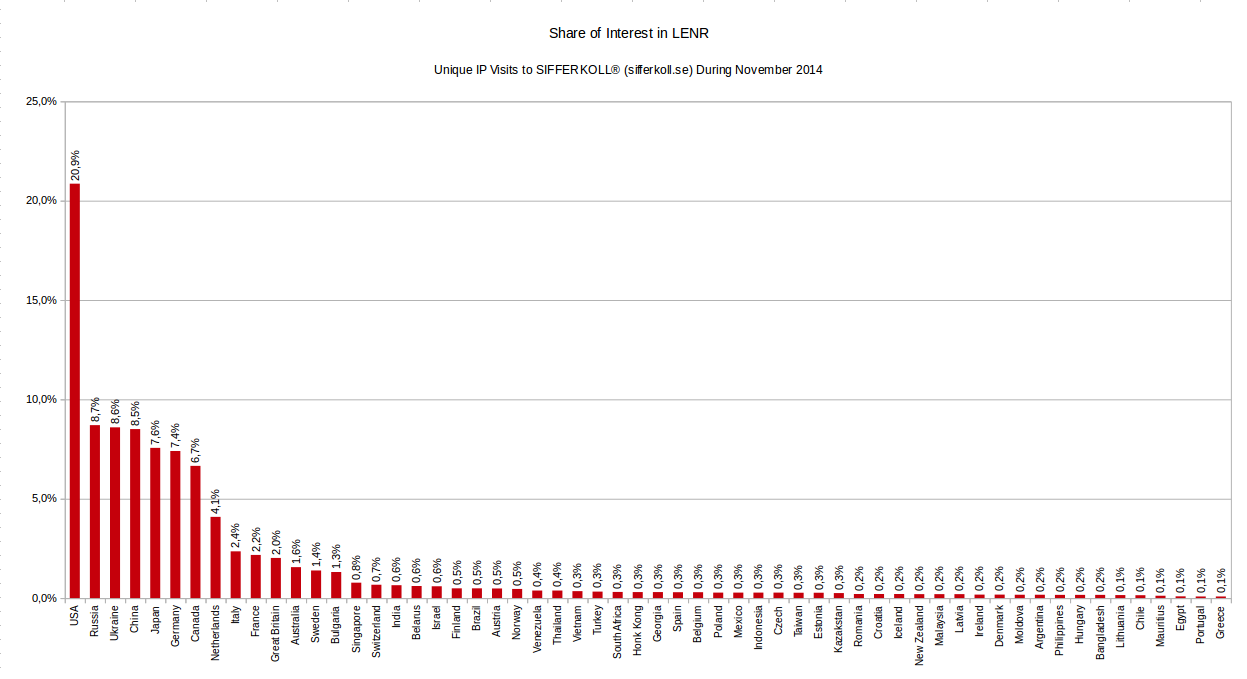

Sifferkoll.se was where the Lugano report on the 32-day test of the E-Cat was first published on October 8, 2014, and the interest turned out to be huge. As of today, the report has been downloaded about 150,000 times. Most downloads are made from the US, followed by Russia, Ukraine, China and Japan (see the diagram).

Sifferkoll.se was where the Lugano report on the 32-day test of the E-Cat was first published on October 8, 2014, and the interest turned out to be huge. As of today, the report has been downloaded about 150,000 times. Most downloads are made from the US, followed by Russia, Ukraine, China and Japan (see the diagram).

So who are all those people? Enthusiasts following the LENR topic? Researchers? Or maybe also some other kind of people?

Ratio between stock index Russel 2000 and oil price since 2012. Note October 8, 2014, when the Lugano report was released.

What Nyberg also noted was that at the exact time of the release of the report, the ratio between stock value (Russel 2000 index) and oil price (USO) took off like a rocket (see the graph). As of December 30, 2014, the increase was +84 percent.

And as you can see in the graph below, this was the first time in 22 years that stocks and oil were decoupled in that manner.

Now, Nyberg has also noted something else, which has not been publicized much. Since 2010/2011, when Rossi’s E-Cat was noticed publicly for the first time, the positions in oil futures and options at the commodity futures exchange NYMEX and the Intercontinental Exchange ICE have changed radically.

Ratio between S&P500 and oil price for the last 22 years.

There are basically four groups on these exchanges, Nyberg told me — oil producers, swap dealers (big banks), managed money (pension and saving funds), and others.

Earlier, oil producers had hedged their sales through contracts with a “short” position (contracts that let you earn money of the price falls). But since 2011, big banks like Goldman Sachs and JP Morgan have essentially overtaken this role. From initially having about 200,000 contracts with a “long” position (letting you earn money if the price increases), they have drastically changed strategy, moving to as much as 500,000 contracts with a short position, together with oil producers, securing the possibility to sale oil at $90-$95.

They have sold some of this but do still have almost 400,000 such contracts. With each contract applying to 1,000 barrels, and at an oil price at $45 per barrel, that corresponds to unrealized earnings of about $20 billion. And yet they seem to keep waiting. Which means that they expect the price to fall further.

The information is public at cftc.gov and yet few have commented on it. Nyberg wrote a piece on his findings on Oilprice.com two years ago, without much people picking up this data, although the post has had 38,000 hits by now. And since then the change has only been reinforced, Nyberg says.

The hypothesis is that big banks know about the E-Cat and LENR since 2010 (possibly because Rossi might have had early contacts with U.S. military), and that they act on this information but want to keep it secret as long as possible. The longer they can maintain the information advantage, the bigger gain they can make the day LENR reaches public awareness and oil price plunges to almost zero.

And the losers? Owners of large oil fields — mostly nations and oligarchs. And “Managed money” — i.e. savings and pension funds — that have long positions in oil. In other words, you and me.

As Nyberg points out, shale oil is the common explanation for why the banks don’t believe in an increased oil price. But as he also notes, it’s strange that analysts at the big funds don’t come to the same conclusion.

“We’re talking about oil analysts with basically the same job on Wall Street, just with different employers … Yet they make completely different analyses of such a well documented and publicized phenomenon as shale oil. Something must be wrong,” Nyberg says.

And indeed, pulling out the details on the banks’ positioning, together with the timing of the Lugano report, undoubtedly makes an intriguing case.

– – – –

BTW — I’m glad to see that Nyberg found this little mostly unnoticed update in the second edition of An Impossible Invention.

– – – –

This post was updated with the SP500/oil price graph, and a quote by Nyberg on February 2.

– – – –

UPDATE 2: Back in 2012, BlackRock Inc., the world’s largest asset management company, wrote in a report called ‘US Shale Boom: A Case of (Temporary) Indigestion’ (p 11): “We are closely following start-ups experimenting with new technologies such as low-energy nuclear reaction and fusion. If successful, these efforts could completely change the current status quo and hurt traditional energy producers. It is worth watching this space. People tend to overestimate what can be done in a year, but underestimate what can happen in a decade.”

Torkel Nyberg said that the Lugano report was downloaded by Blackrock minutes after it was released in October 2014.

UPDATE 3: Ooops — I forgot to mention the interest in LENR showed by Bill Gates (who received the first copy of my book in Stockholm on March 31, 2014). In November he went to visit ENEA, a renowned LENR lab in Italy, ‘on a personal trip to learn more about the innovative work the agency is doing’, and in the Annual Letter 2015 he was hinting about an energy source such as LENR.

Maybe it was just a coincidence that his close and longtime friend Warren Buffett sold off a $3.7 billion investment in Exxon Mobile during Q4, 2014?